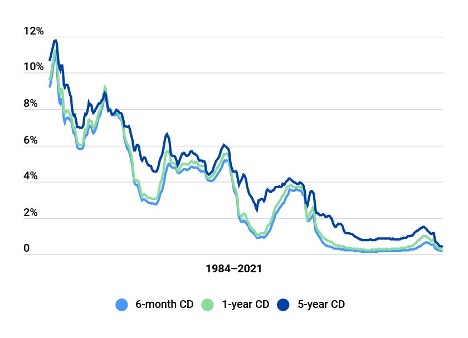

You’re familiar with the concept of interest: you put your money in the bank, the bank pays you for the use of that money. In the olden days of yore

12k

By Shantun Parmar

You’re familiar with the concept of interest: you put your money in the bank, the bank pays you for the use of that money. In the olden days of yore (the 1980s), you could earn over 10% interest by keeping your money in the bank, but today it’s less than 1%.

So if inflation is running at 7%, then simple math shows us that .06% interest rate – 7% inflation = -6.94%. In other words, keeping your money in a traditional banking account means you’re slowly losing money: year by year, it’s being eaten away by inflation.

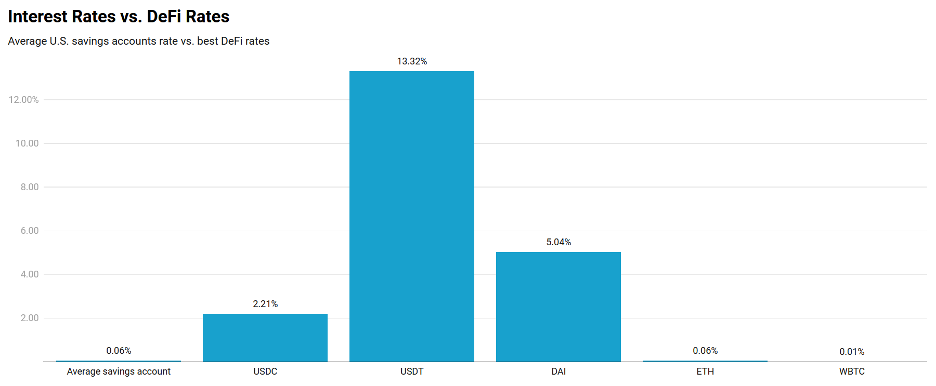

Holding your savings in cryptocurrency can offer much higher interest rates, allowing you to meet or beat inflation. In this article, I’ll explain the three common ways of earning interest (crypto sites call it “yield”), along with how to do it.

But first, some practical advice.

How to Tell Whether a Crypto Interest Rate is “Real”

You’ll see all kinds of crazy interest rates on crypto sites. 10% APY. 100% APY. (This means you’d double your money after a year.) We’ve even seen claims of 12,000% APY (for a limited time only).

Here are some simple rules of thumb.

If it seems too good to be true, it probably is. Sky-high interest rates (let’s say anything over 10%) are usually new projects trying to attract users. The APYs won’t last, and the projects are risky. Stay away.

The “yearly” APY is not actually locked in for a year. Because APYs are calculated real-time on supply and demand, tomorrow’s APY may be different. But this is the way traditional banks calculate it, even though it’s misleading.

What is APY in crypto? APY, or Average Percentage Yield, is a term borrowed from traditional banking. It refers to the amount of interest you’ll earn in a year, including compounding interest. Like banks, APYs can change at any time – but because crypto is more volatile, they can change radically.

With greater reward comes greater risk. We’ve listed only the most reputable sites below, which have a track record of safety. The rule of thumb is to look for more established platforms (several years in business) with plenty of users (several million).

Earning interest on crypto is legal, but unregulated. Because crypto is generally not regulated like banks, you always stand a small chance to lose your money. You may be better off just holding your bitcoin and Ethereum yourself, and letting them grow.

Your “interest” is often paid in another token. Imagine putting money into a Bank of America savings account and getting “BankBucks” in return. You can still redeem BankBucks for U.S. dollars (for a fee), but the price of BankBucks will go up or down, as if it were Bank of America stock. That’s crypto.

Fees are the silent killer. To participate in these crypto platforms, you’ll need to pay Ethereum “gas” fees (i.e., service charges). You will never hear crypto sites tell you about the fees, which can easily eat all your profits, and then some.

Your interest is taxable. Finally, depending on the platform you’re using, the tax obligations can be confusing. Rule of thumb: you’ll be taxed for any token bought and sold for a profit, as well as any interest income you received. (Here’s a crypto tax guide.)

So, with all this, is it worth it?

For small amounts of money (let’s say anything under $1,000), you might be better off just holding it in bitcoin or Ethereum, and letting them grow.

If you do decide to earn interest, then think long-term (5+ years). The outrageously expensive fees to move your money in and out, as well as the tax implications, mean that you’ve got to be really patient to make money with interest.

But if you’re willing to wait, you really can earn interest on cryptocurrency, at rates far more attractive than any bank. Here’s how.

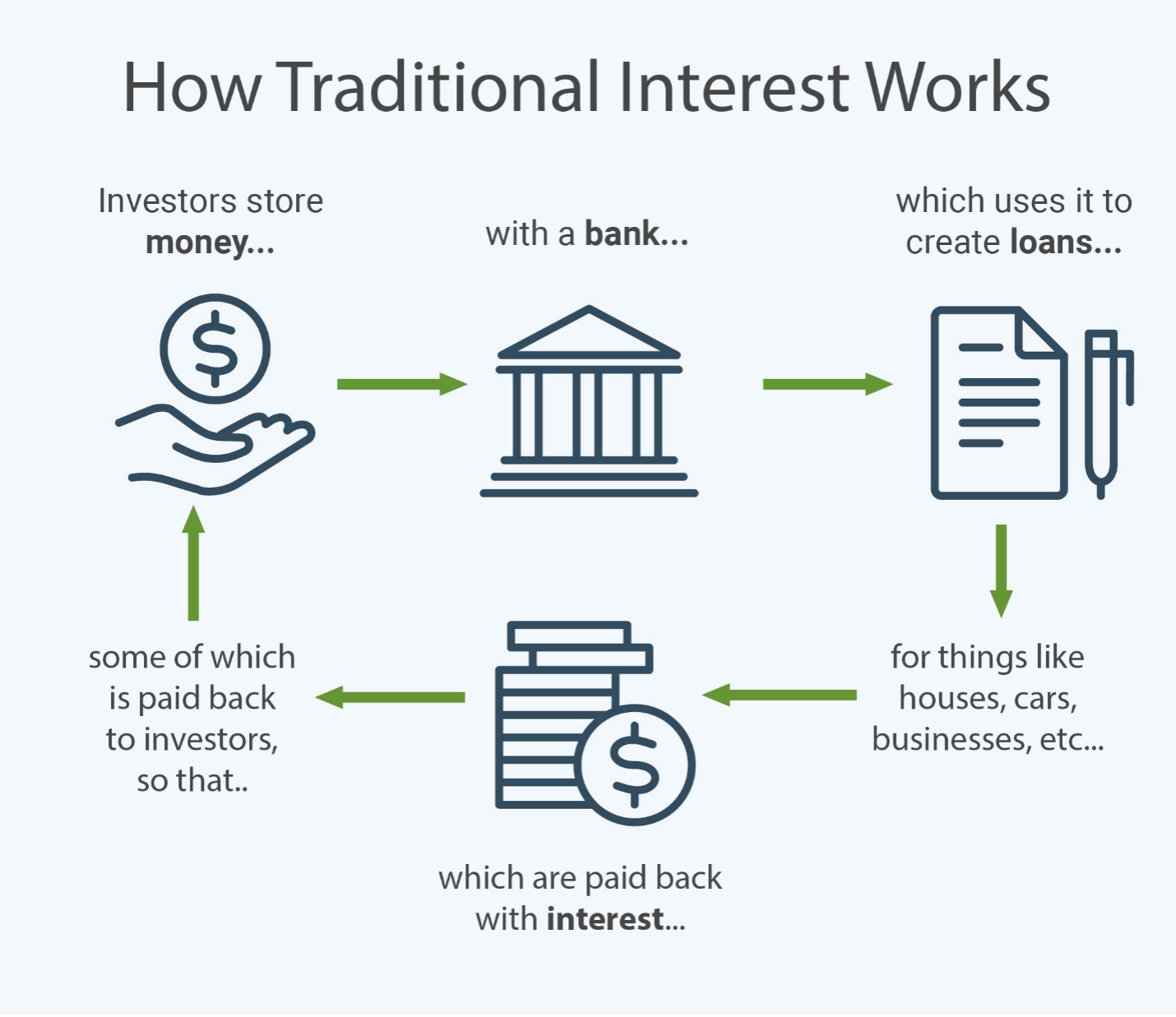

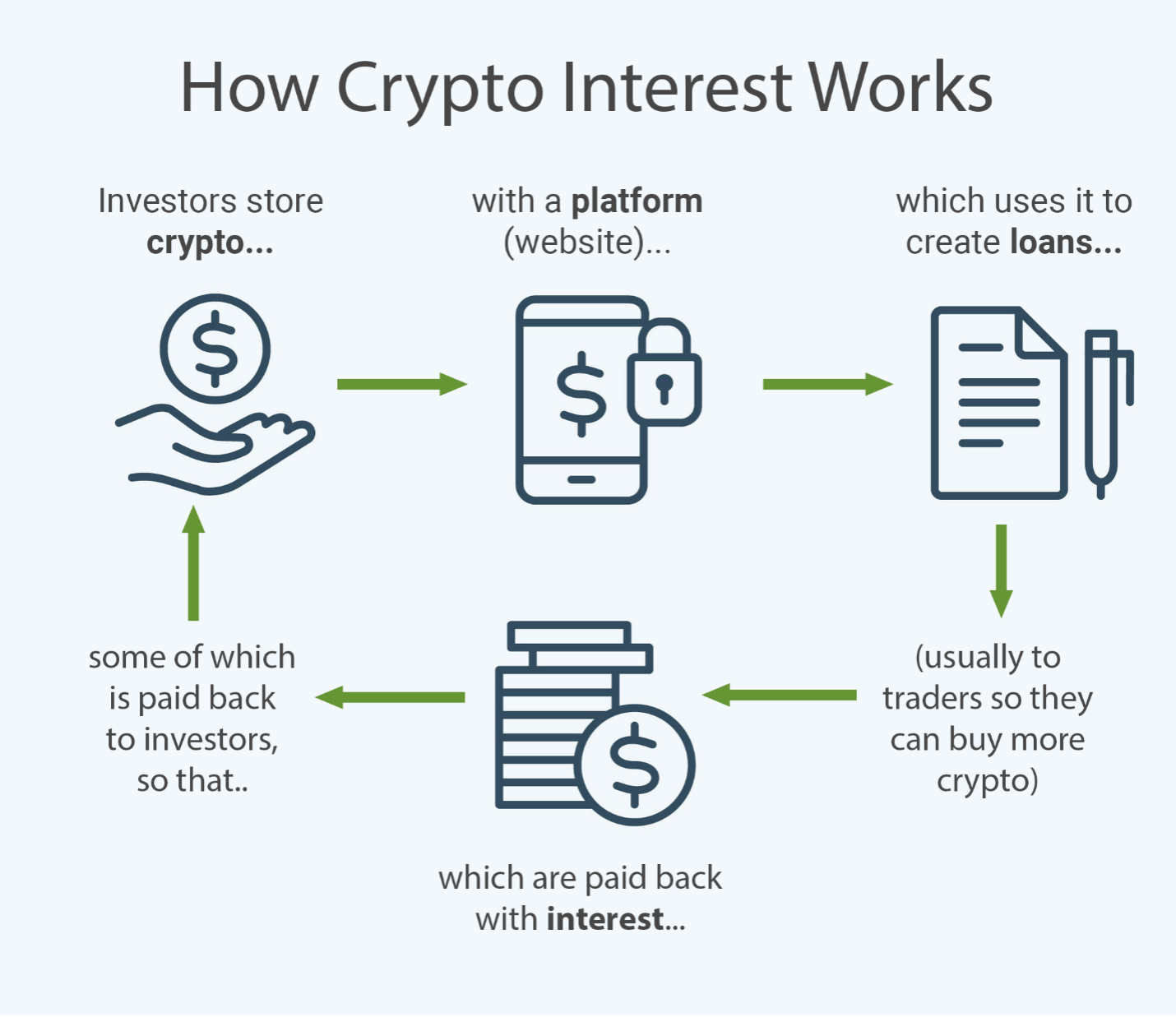

1) Lending. This is the most common method of earning interest on your crypto investments: loaning your crypto to other people who can borrow it. You never see these people: it’s all handled through online lending platforms.

As an analogy, it’s like depositing money in a traditional savings account. The bank pools together money from customers and uses it for loans. The bank makes money through the interest from the loans, and some of that interest is paid back to customers.

Crypto lending platforms work essentially the same way: you’re putting money into a “lending pool,” which borrowers can use to take out loans. They pay back the loans with interest, which is distributed back to lenders.

Who’s borrowing this cryptocurrency? Mostly traders, who use the extra money to make bigger and riskier bets. However, this risk is generally not passed on to you, as the borrowers have to overcollateralize (or back up their loans with even more crypto), which will be automatically sold and paid back to you if they end up making a bad trade.

This may all sound like a house of cards, but so far it has worked surprisingly well. Even when crypto markets have had sudden crashes, the automated “circuit breakers” (also called “automatic liquidations”) will sell the collateral and pay back the lenders.

As the lender, you just keep earning interest. This all happens behind the scenes.

This doesn’t mean lending is entirely without risk: sometimes hackers will find bugs in the code. Again, the rule of thumb is to look for platforms with several years in business and several million users, which are good indicators of whether their platforms are ready for prime time.

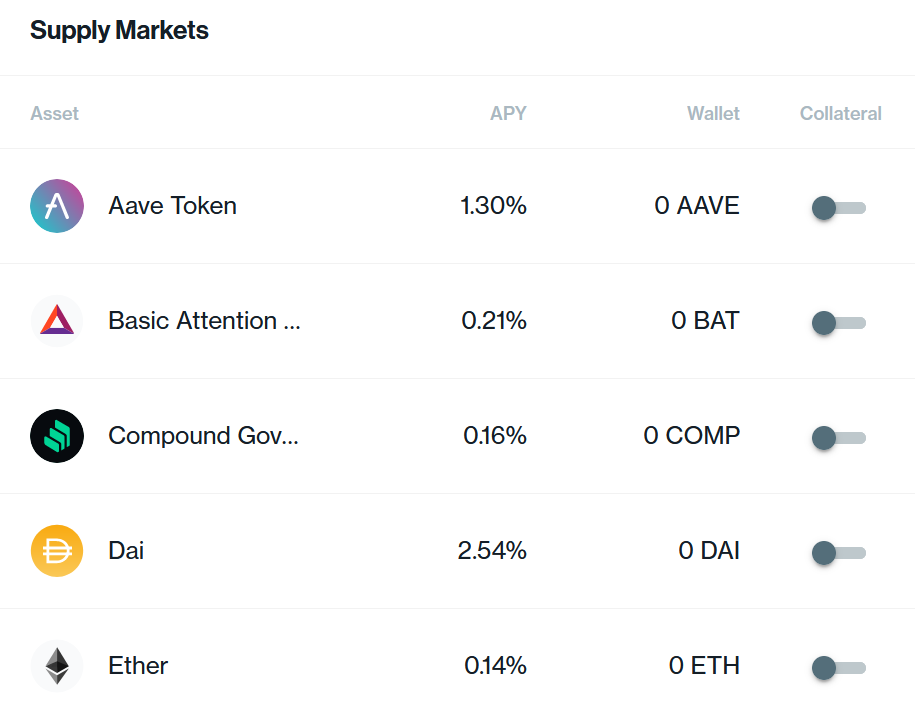

How to do it: First, you need to buy cryptocurrency (we recommend Coinbase or Binance), then move it to a browser-based crypto wallet (we recommend MetaMask). You then navigate to a lending site (the most popular is Compound), and “lock up” your crypto as “collateral”:

To loan your crypto, you just switch on the “Collateral” slider. It’s that easy.

You can withdraw your money at any time: unlike CDs, there is no lock-up period. Again, however, you will pay Ethereum fees when you deposit crypto, and when you withdraw crypto. You’ll see these fees before you approve the MetaMask transaction. (See our article on How to Avoid Crypto Fees.)

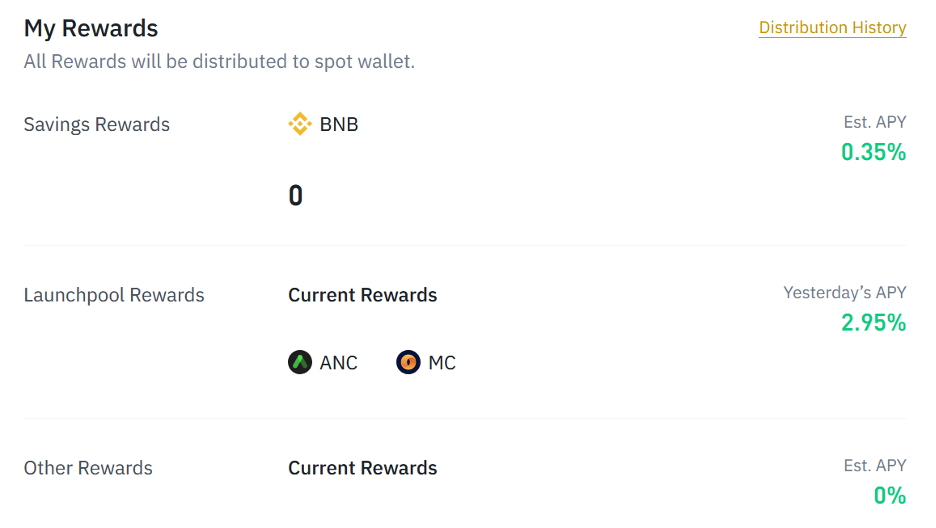

2) Staking. This is the second way of earning interest on your crypto investments, like storing your money in a savings account. In crypto platforms, the “staked” money helps keep the network running, by validating transactions and pays you interest in return.

As with lending, this “interest” is usually paid in the platform’s own token—and they want you to stake that token, too. For example, the crypto exchange Binance has its own Binance token (BNB), which you can stake in its platform (called “Vaults”). The revenues that Binance earns on its platform — when people make trades — are then distributed back to stakeholders: that’s your “interest,” paid in BNB.

3) Providing Liquidity. The third way of earning interest is for advanced users only. You need to be tech savvy, with more free time and a tolerance for risk. This is not a “set it and forget it” approach, but interest rates can be much higher.

Crypto exchange sites like Uniswap are called Automated Market Makers (AMMs). Think of the exchange kiosk at the airport that lets you swap dollars for, say, Euros:

Using an AMM, anyone can swap one token for another (say, ETH to USDC) instantly, within their browser. Of course, you can do this at an exchange like Binance, but with services like Uniswap, users are providing the funds (or “liquidity”) on the other side, rather than Binance. It’s peer-to-peer.

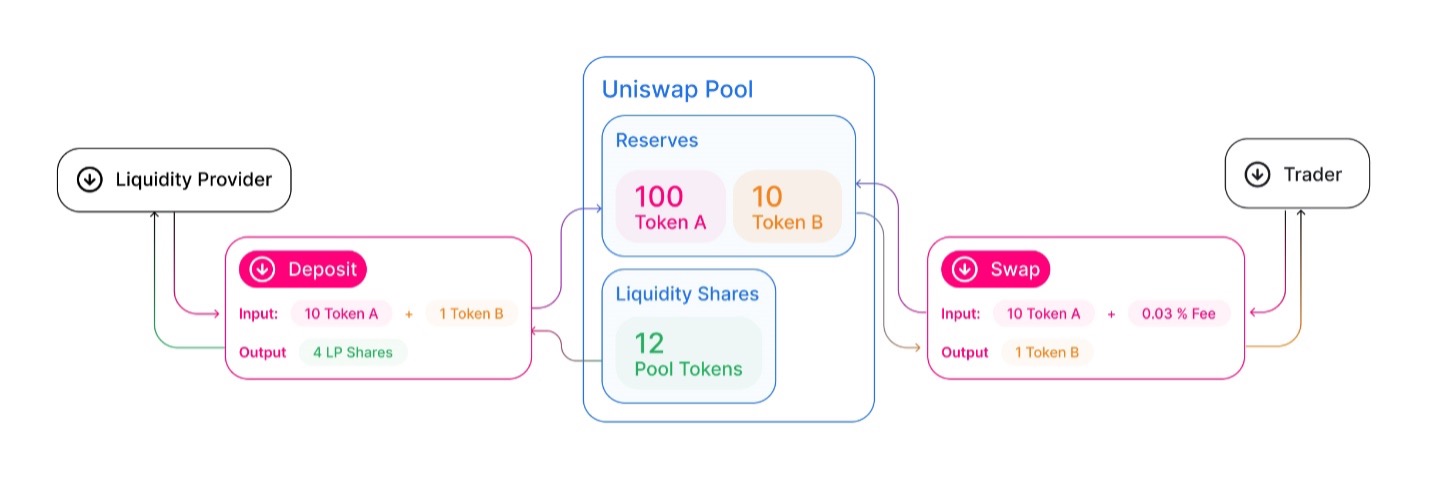

If you’re providing the funds for the trades (or “swaps”), then you are a Liquidity Provider (or “LP”). In essence, it’s like you’re the airport exchange kiosk.

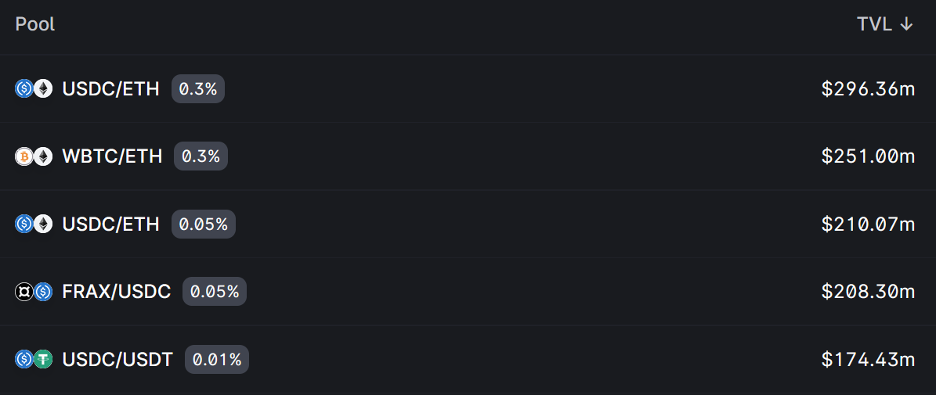

As with lending, you’re never seeing the people making the swaps: you just lock up your crypto in Uniswap “pools”, and the platform handles everything behind the scenes. You receive a chunk of the service fees generated by the swaps.

The percentage at left is sample APYs you’ll earn from contributing to these lending pools. The number at right is how much money users have already locked up in these pools. (Real-time stats here)

Given that swapping one token for another is one of the most common use cases for crypto, there is a lot of money to be made here. But again, with more reward comes more risk, and there is one huge risk that is misleadingly called “impermanent loss.”

Savvy Liquidity Providers, then, are not a “set it and forget it” type of crowd. They’re monitoring price movements and trying to get out while they’re still ahead—which in the wild world of cryptocurrency is easier said than done.

As a LP, you’re providing the crypto for the trade, and earning “interest.” (Courtesy Uniswap)

Yield Farming: Harder than Regular Farming

All these strategies are sometimes called “yield farming,” or hopping around from platform to platform, constantly chasing the highest interest rates. Between the research required, the sky-high fees, and the tax and accounting headaches, this is rarely worth it. It’s easier to stick with one interest-bearing platform for the long term.

People do “yield farming” in the traditional banking system, too. They’d move their money from bank to bank every few months, for another percentage point or two of interest. In the end, you have to ask if that’s really the road to wealth, or if your time could be better spent elsewhere.

(Note there are also platforms that will do the “yield farming” for you, with the promise that if you lock up your cryptocurrency, they’ll find the best rates automatically. The jury is out on whether this creates “taxable events” every time the platform buys and sells for you. Again, set it and forget it.)

Download Our Crypto Interest Rate Calculator

We’ve put together a crypto interest rate calculator, which can give you a rough estimate of how much you’ll really be earning with that too-good-to-be-true crypto APY. It figures in length of time, gas fees, and tax liabilities, with easy-reference numbers that you can customize. Blockchain Believers can download it here.

In summary: Crypto interest rates are real, and can pay much better than a bank – but beware of offers that seem too good to be true. Use established platforms with good reputations. Think long term. Don’t forget taxes and fees. Then, set it and forget it.